United India Insurance is one of those general insurance providers in India that hold a reputed name in the insurance industry owing to being one of the oldest and trusted names. This central public sector undertaking is owned by the government of India and has been safeguarding the lives of millions of policyholders since 1938: from bullock carts to satellites. In this elaborate 2026 guide, we will discuss the company overview, products and features, claim settlement track record, solvency ratio and everything else you need to know before purchasing a policy from them.

It is a detailed article which you can use to get a complete and impartial information of United India Insurance whether you are someone looking for your first policy, an existing policyholder or someone comparing insurers. By the end of this, you should clearly know what the insurer is all about, where it excels and where you need to think twice before signing on the dotted line.

About the United India Insurance Company

United India Insurance Company Limited (UIICL) is a nationalised general insurance company owned by the Government of India and based in Chennai, Tamil Nadu. Founded in 1938, the company has also been a key player when the nationalisation of general insurance sector took pace in the country in 1972. At the time of nationalisation it had amalgamated with 12 insurers in India, the Indian operation of five foreign-based insurers, four cooperative insurance societies and the LICof India.

At present, United India Insurance is fourth biggest public sector general insurer in the country. The company operates with a 18000-plus workforce consisting of more than 1 crore policyholders from urban centres and rural communities, developing an efficient distribution network. This one of the most recognised insurers in the country thanks to its reach and legacy.

The firm has even pioneered rural insurance businesses, ensuring coverage for underserved communities. The product range is impressively diverse, ranging from agricultural risks to aviation and even space insurance. The capacity to create and execute the complex insurance policies for big clients, while at the same time being in service of a common citizen, is what has given the insurer a place on earth over its more than 80 year history.

Quick Company Overview: United India Insurance

Below is a quick summary of this company.

| Particulars | Details |

| Company Name | United India Insurance Company Limited (UIICL) |

| Founded | 1938 |

| Nationalised | 1972 |

| Headquarters | 24, Whites Road, Chennai, Tamil Nadu – 600014 |

| Ownership | Government of India (Public Sector Undertaking) |

| Type | General Insurer |

| Employees | 18,000+ |

| Policyholders | Over 1 crore |

| Website | uiic.co.in |

| CRISIL Rating (2025) | AA- |

The following snapshot illustrates why United India Insurance has managed to retain its household name even as many private players burst on to the scene in the last twenty years. It is a great example of company that combines scale, state ownership, and long history.

Read Also:- What is the Right Age to Purchase a Health Insurance Policy?

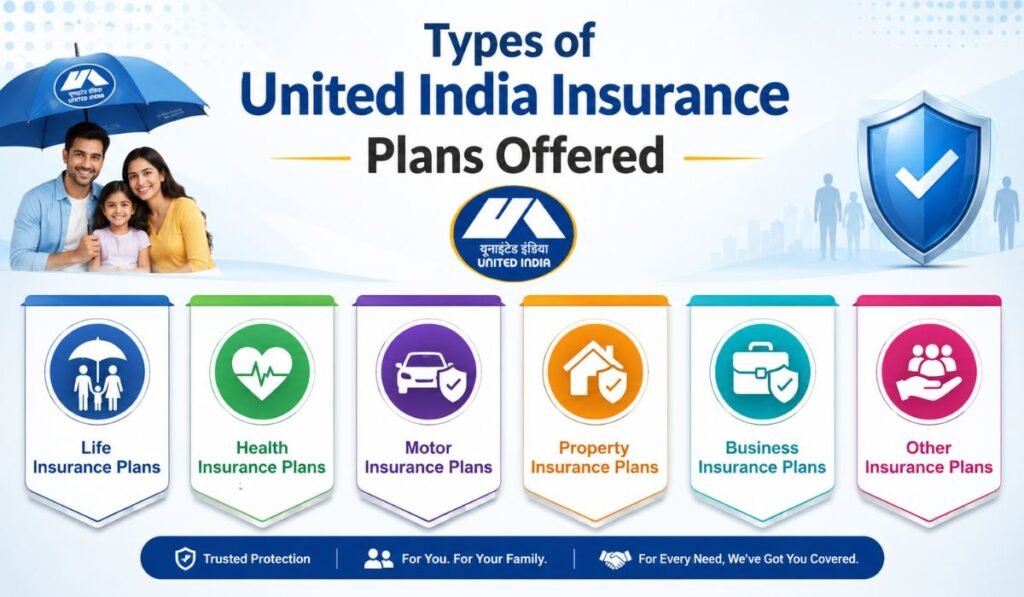

Types of United India Insurance Plans Offered

The diversity of product portfolio is one of the major strength of company. There is plentiful plans available here, whether you want to cover your health, protection of vehicle, home or business. Now, let us delve into the key categories.

Health Insurance

United India Insurance provides a lot of insurance plans and health coverage is one of its most sought-after offerings. This company comes with much variety of plans that it has designed for individuals, families and elderly citizens. Key health products include:

- Family Medicare Policy – An extensive floater policy that covers a complete family under 1 sum insured which also includes hospitalisation and AYUSH treatment.

- Individual health insurance policy – These are meant for single policyholders who wish to be solely insured.

- Senior Citizen Health Insurance Policy – Designed for the senior-most citizens (aged 60 years and older) with suitable plan-specific features.

- Super Top-Up Medicare Policy – A product which has won several awards that offers added cover beyond a base health policy at an economical premium.

- The Unimedicare Policy: A simple health plan that covers hospitalisation costs like room rent, surgeon fees, anaesthetist charges, medicines and blood use as well as oxygen.

- Critical Illness Insurance – It pays a lump sum if you are diagnosed with any specified life-threatening diseases.

They usually also cover hospitalisation, pre and post hospitalisation expenses, daycare procedures and ambulance charges. The extent of finding themselves in the AYUSH (Ayurveda, Yoga, Unani, Siddha, Homeopathy) fold shows that the insurer remains mindfully cognizant of how healthcare is best perceived in India. Was industry recognised as the most innovative product of 2023 with its suite of products, specifically its Super Top-Up Medicare Policy, which enabling customers to increase their total coverage by hundreds off thousands for only a small premium compared to a standalone high-sum-insured plan.

Room rent cap, disease wise sub-limits, waiting period for pre-existing diseases and no-claim bonus are some of the features customers must consider while selecting a health plan Reading the policy wording carefully can prevent surprises at the time of a claim.

Motor Insurance

Motor insurance policies offer just that among others, but a vehicle owner can select one. It provides comprehensive and third-party liability cover for cars, two-wheelers & commercial vehicles. Notable products include:

- Car Insurance – Contains appealing add-ons like zero depreciation, engine protection and roadside assistance at an extra premium.

- The Motorcycle and Scooter Package Policy: It provides for an all-in-one, one-year coverage (for both own-damage plus third-party) for two-wheelers.

- Commercial Vehicles Package Policy – This type of policy is for goods carriers, passenger vehicles, taxis and other types of commercial vehicles.

Along with this, United India Insurance motor coverage also offers compulsory third-party liability which is mandatory for all vehicles running on Indian roads. However, comprehensive plans do more for you by covering your own automobile from blooming damage, authorized exertion, and natural disasters. Thanks to add-on covers, policyholders can tailor their coverage in accordance with their driving behavior and the worth of their car or truck.

Travel Insurance

The company offers travel policies that safeguard frequent traders from experiencing unexpected events during domestic and international journeys. This is one of the more acquired travel products across the country. It includes medical treatment costs overseas as well as loss/delay of checked-in baggage, theft or loss of passport, trip delays, hijack cover, personal accident, personal liability and missed connections. And, if you are travelling for business, leisure, education or pilgrimage – that kind of coverage gives peace of mind.

Home and Property Insurance

Another important segment that we offer is Home and property protection by United India Insurance. A Householders Policy, is an all-in-one insurance plan that covers different cover under one roof against the building structure, contents and valuables with a personal accident cover of family members as well. Business owners have the option to choose Shopkeepers Insurance Policy, which covers business premises and goods against fire, theft and other perils. These combination offerings are convenient because they roll up multiple coverage types into one easy to manage product.

Personal Accident and Other Plans

Apart from the core categories, personal accident cover, marine insurance, crop insurance, fire insurance, engineering insurance and liability insurance are other products offered by the company. This is the range of products with which the company is often described as providing insurance “from bullock carts to satellites”. The partnership includes an array of specialist insurance solutions for farmers, manufacturers and exporters as well as large corporates — a reflection of the versatility and breadth of cover the insurer can provide.

Product Portfolio Summary of United India Insurance

This table offers a handy roadmap for the major types of insurance and their essentials.

| Insurance Category | Key Plans | What It Covers |

| Health Insurance | Family Medicare, Super Top-Up Medicare, Senior Citizens, Unimedicare | Hospitalisation, daycare, AYUSH, critical illness |

| Motor Insurance | Car Package, Two-Wheeler Package, Commercial Vehicle | Own damage, third-party liability, add-ons |

| Travel Insurance | Overseas Mediclaim, Domestic Travel | Medical costs, baggage loss, trip delays |

| Home Insurance | Householders Policy | Building, contents, valuables, personal accident |

| Business Insurance | Shopkeepers, Fire, Marine, Engineering | Property, stock, liability, transit |

| Personal Accident | Individual & Group PA | Death, disability due to accidents |

This wide aggregation allows most consumers to find a roof for their needs. The range of choice here is one of the key attractions for buyers who want to source all their insurance needs from a single established provider.

Read Also:- What Is a Corporate Insurance Policy and Its Benefits ?

United India Insurance Claim Settlement Ratio and Performance

One of the most important aspects in assessing any one insurer is its claims settlement ratio. As per the latest data, United India Insurance has a favorable average claim settlement [till FY 2022-25] ratio of 93.79%, which is decent for any public sector insurer. That means that for every 100 claims received, about 94 got paid out which is a good sign showing the company is not a scam.

But prospective buyers should be aware of one significant caveat. Its incurred claim ratio (ICR) was 98.77% in FY 2022-25, a clear indication of financial trouble for the debt-wicked firm. This means the insurer is basically paying out as much in claims as it collects in premiums, which can put long-term profitability under pressure and something that is worth monitoring over time.

The scale of operations is quite extensive in terms of the volume of claims. The insurer’s gigantic footprint in the Indian market is clear from the fact that it issued 90,65,571 policies in FY22-23 and a total of over 46,14,549 claims. Even at this scale, dealing with claims takes a huge operational machine and an extremely robust administrative network.

Claim Performance at a Glance

| Metric | Value (FY 2022-25) |

| Average Claim Settlement Ratio | 93.79% |

| Incurred Claim Ratio (ICR) | 98.77% |

| Claim Loading on Renewal | None (as per IRDAI rules) |

It deserves notable mention that IRDAI regulations and the policy wordings offer that there will be no loading (extra premium charge) on renewals based on individual claims experience. With this consumer-friendly rule, your premium does not go up just because you filed a claim the year before. Your renewal premium would only change if you have entered a new age band, there is a revision in the base rate approved by IRDA or any modifications on the sum insured.

Financial Health in 2026

Though the claim settlement ratio is impressive, the financial health of the company should be looked at vigilantly. United India Insurance is also one of the oldest general insurers in India being a PSU owned by the government and founded in 1938. Though it has a solid average claim settlement ratio of 94%, but has to deal with severe financial stress at -0.65 solvency ratio in 2025, much below the regulatory limit.

Solvency Ratio– The solvency ratio is an indicator of the ability of an insurer to meet its long-term obligations. The minimum required by the regulator is 1.50. Both its capital buffer has now gone into negative territory and this means that Not only is the company not even close to fulfilling their minimum solvency ratio (1.50) requirement but also does enjoy any buffer at all as its liabilities out weigh assets, or surplus leaving no room for error in financial terms. This casts doubt on its capability to honour future claims without obtaining more capital from third parties.

But there is some good news. In FY25, the insurer lost ₹154 crore but returned to a net profit. Coming back to profitability after a few years of losses is an encouraging reversal. Also, in the context of digital transformation and improving customer service at public sector insurers nearing an increasingly tech-driven marketplace, many have now urged the Finance Minister too.

We should call your attention to another item development — the credit rating. The company’s rating was downgraded from AA to AA- by CRISIL Ratings. A downgrade to AA- is still an investment-grade rating and indicates a strong credit risk, but it signals some of the financial pressures that the company is managing. The downgrade, however, needs to be interpreted in the spirit of a warning not a panic as investment-grade ratings still show that there is a high degree of safety when it comes to timely servicing of financial obligations.

Key Financial Indicators

| Financial Metric | Status (2025) |

| Net Profit FY25 | ₹154 crore (return to profit) |

| Solvency Ratio | –0.65 (below regulatory minimum of 1.50) |

| CRISIL Credit Rating | AA- (downgraded from AA) |

| Market Position | 4th largest public sector general insurer |

However, since it is a state-owned insurer, United India Insurance receives solid implicit backing from the government. Traditionally, when the government has intervened with capital top-ups to bolster public sector insurers, this gives a sense of solace to risk-averse clientele.

Recent Developments and Merger Talks

Late in 2025 saw news of a possible consolidation in the public sector insurance space. The merger proposal for this company and National Insurance was revived by the Finance Ministry along with Oriental Insurance. The merger will change the landscape of public sector general insurance in a big way and also enable the combined entity to strengthen funds by pooling up resources, cutting down on duplicate costs and improve solvency.

The firm also has been establishing new distribution partnerships. With AU Small Finance Bank: Now, a strategic alliance enables the customers of AU Small Finance Bank to avail general insurance services at their Banking Channel. These kind of bancassurance tie-ups help widen the net of the insurer and increase outreach for policies for all consumer segments, especially in places where banks have a considerable reach.

In the leadership team, Bhupesh Sushil Rahul is appointed CMD to provide a fresh story for turnaround time ahead. We typically think about new leadership as a renewed effort and more attention to operational efficiency, better overall customer experience and the digital initiatives that regulators have been pushing them towards.

Read Also:- Policy Bazaar: India’s Largest Insurance Marketplace

How to Buy a Policy from United India Insurance

Procurement of policy from United India Insurance is a hassle-free and straightforward process which can be done through multiple mediums:

- Official Website – Visit uiic.co.in, navigate to the “Products” tab, select “Buy New Policy/Get Quote,” choose your coverage type, enter the required details, and obtain an instant quote.

- Branch Office – Visit any of the company auditars several branches at India to get a guide in person.

- Insurance Agents – Licensed agents can help you compare plans and make the purchase.

- Online Aggregators – Web aggregators and brokers also help to buy and renew policies.

- Bancassurance Partners – via partner banks like AU Small Finance Bank.

For renewals, existing customers can easily log into the customer portal on the official website of Cabot and can simply manage & renew their policies. Keep your policy number and registered contact details handy for a smooth and rapid process.

United India Insurance claim process

United India Insurance claim process will vary as per the different types of policies. But, below are the general steps for a health insurance claim.

To settlement of your claim cashless to make a claim, you must avail treatment at the network hospital along with health card and ID. The TPA will directly coordinate with the hospital for settlement This means you will not have to pay a heavy amount from your pocket for planned and emergency treatments at the listed hospitals.

Your endeavour SRV is the claim two types of policy are reimbursement claims and Carer insurance, you will pay the hospital bills at front then file a claim thereby submitting a claim form along with copies of all original documents such as hospital bills, discharge summary, diagnostic reports & prescriptions to insurer or Third Party Administrator (TPA) in order to process claim. It is however wise to keep photocopies of each and every document you send for your own records.

United India Insurance, like its public sector counterparts utilise TPAs to process claims for both group and retail insurance. This may be a common industry practice, yet the extra steps that TPA-managed processes can require — compared to in-house claim teams via insurers for example — still leaves customers needing to brace themselves. The one single best way to avoid delays is to inform the insurer promptly and submit complete, accurate documentation.

You need to notify the insurer within the time frame mentioned in your policy document for all claim types; otherwise, there may be a delay or rejection. It is best suggested to meet the claim intimating timelines at the time of buying instead of an emergency.

Advantages of Choosing the Insurer

Here are a few reasons why this insurer continues to inspire customer trust:

- Long history – Almost nine decades in business since 1938, giving us vast experience and consistency.

- State Support – It is a public sector undertaking and will be benefitting from the implicit government support from Government of India.

- Healthy Claim Settlement Ratio: An average of 93.79% is a good sign for the insured,

- Diversity in Products – Health and motor as well as marine and crop insurance are relatively broad.

- Broad Network – Expansive branch and hospital network across the cities of urban and rural India

- No Claim-Loading—You will not be penalised by the fact that you made a claim.

Such strengths should give United India Insurance a competitive advantage among line-seeking buyers looking for stability and trust rather than lot of frills from the latest in digitalisation. Still, for many Indian households, the fact that it’s an established government-owned company wins out over all those other considerations.

Points to Consider Before Buying

On balance, there are many beneficial features but this warrants a comment on the limitations too.

- Financial Stress – The solvency ratio is negative which means that company’s liabilities exceed its assets, along with the CRISIL downgrade these are concerns.

- TPA Dependency — Claims are administered through third-party administrators, perhaps introducing a few steps.

- Lack of Modern FeaturesSome plans do not offer modern features like restoration benefit or impose room rent cap and disease specific sub-limits.

- Premium Pricing – Premiums might be a bit on the costly side in comparison to certain private competitors that provide richer features.

Balancing these factors with the advantages will only you make that United India Insurance is suitable for your particular situation and risk appetite. However, before you decide which provider to choose, it is always a good idea to get the features, premiums and exclusions compared between two or three insurance companies carefully.

Comparison: Public Sector Insurer Pros and Cons

| Pros | Cons |

| Long-standing legacy since 1938 | Negative solvency ratio in 2025 |

| Government ownership and backing | Recent CRISIL rating downgrade |

| Healthy 93.79% claim settlement ratio | Dependence on TPAs for claims |

| Broad and diverse product portfolio | Some plans lack modern features |

| No premium loading on claims | Premiums comparatively higher |

The result should help you choose wisely for your 2026 coverage needs with this insurer. When it comes down to which insurer is best for you, options will be determined based upon what your priorities are, cost-effectiveness and what risks you want covered.

Read Also:- Max Life Insurance

Who Should Consider This Insurer?

Best suited for United India Insurance

- Those conservative buyers who place a premium on the stability and credibility offered by a government-owned company versus shiny private-sector frills.

- Rural and semi-urban customers who gain from the extensive branch network and grassroots presence.

- This is for vehicle owners looking forward to reliable motor coverage along with well-established add-on options.

- The comprehensive floater health plan such as Family Medicare which is for 2 or more people.

- One Trusted Provider To Get Fire, Marine, Engineering And Shopkeeper Covers For Business.

If you emphasise longevity and security with a full state guarantee, the insurer is still a reasonable alternative. But, for anyone looking for plan features and possibly the fastest digital claim experience available, it might be worth comparing closely with top private insurers prior to choosing. Brand loyalty alone is not as important as matching the product up to your real world needs.

Tips to Get the Most From Your Policy

These practical hints will help you get the most out of any policy you purchase. Firstly, be very upfront with your medical history and any pre-existing conditions at the point of purchase; non-disclosure is one of the most common reasons for rejection. Second, arrive at a correct sum insured that represents current day hospitalization and replacement costs rather than an amount which looked comfortable 10 years back. Third, know the waiting periods, sub-limits and exclusions before purchase rather than after.

Fourth, renew your policy on time so that you do not lose out to continuity benefits like a no-claim bonus and also avoid the pressure of waiting periods being reset. A few simple steps to ensure that you butt coverage actually performs when you need it.

FAQs about United India Insurance

Q1. Is United India Insurance a government company?

Yes. United India Insurance Company Limited (UIIC) is an Indian nationalised non-life insurance company owned by the Government of India. Nationalisation happened in 1972 and it remains in state ownership today.

Q2. What is the claim settlement ratio?

The claim settlement ratio of the company stands at around 93.79 per cent on average during FY 2022-25 which is good for a public sector general insurer.

Q3. Is United India Insurance financially safe in 2026?

FY25: The insurer made a net profit of ₹154 crore Nevertheless, it posted a solvency ratio of –0.65 in 2025 — below the regulatory minimum (1.50) and prompting CRISIL to downgrade its rating from AA-. While the government backing is reassuring, buyers need to consider these financial aspects critically.

Q4. What types of insurance does the company offer?

It provides health, motor, travel, home and personal accident insurance as well as marine, fire, crop, engineering and liability cover with specific group and commercial products.

Q5. How can I renew my policy online?

To renew the policy visit and login into the customer portal on official website. with the option to pay directly through UPI or PayPal once you have entered your policy details.

Q6. Does the insurer offer cashless hospitalisation?

Yes. The said company provides cashless treatment at their network hospitals via Third Party Administrators (TPAs). You have a cashless settlement by showing your health card at a network hospital.

Q7. Will my premium increase if I file a claim?

No. No loading based on individual claims experience for renewals as per IRDAI regulations and the Company’s policy wordings. Your premium can only change based on age, sum insured or if base rates were revised.

Q8. Where is the company headquartered?

Its corporate office is located at 24, Whites Road, Chennai, Tamil Nadu – 600014.

Q9. Is a merger of public sector insurers planned?

The Ministry of Finance has mooted again the merging proposal for this company and Oriental Insurance along with National Insurance. What remains to be seen is the eventual result, but such a merger would presumably bolster the finances of the combined firm.

Final Verdict

To summarise, United India Insurance is one of the oldest and most stable general Insurer in the country with an extremely large portfolio of products (almost entire range) supported by experience of nearly nine decades and ownership structure by Government. Its claim settlement ratio is a robust 94% and the new profitability in FY25 provides comfort over its path ahead.

However, the negative solvency ratio and the CRISIL rating downgrade are real issues which new policyholders need to take serious note of. The company’s domestic market of public sector insurers’ potential merger and the ongoing digitization initiatives can always solidify its position ahead of time, situation to be followed till 2026 and further on.

Whether this insurer is the right pick for you ultimately depends on what you value most. If stability, trust and a wide selection of products is your priority, it’s still a solid and proven bet through 2026. As ever, compare policies, check the policy wording and get qualified guidance before proceeding any further.