Car insurance in India has become an integral aspect of owning a car. With the increase in our Indian roads traffic on 2026, the new challenges such as accidents and theft of vehicles along with natural disasters and third party liabilities. Be it a hatchback, a premium sedan, an SUV or an electric vehicle – an appropriate car insurance policy can help save you from huge financial losses.

Most vehicle owners still perceive car insurance as just a legal requirement. And though one cannot deny that Indian law makes a provision for third-party insurance on every registered vehicle, car insurance has evolved beyond what is legally required from modern options. A full coverage protects your vehicle from any unforeseen event like collisions, floods, fires, theft & vandalism.

Car insurance today has come a long way with the years, given how insurers in India are providing numerous policy choices along with add-on covers, digital claims settlement service, and AI-based customer support. If you know how car insurance works, you can find the coverage that is right for you and avoid overspending on your auto policy or leaving your vehicle unprotected.

An extensive guide that explains everything you should know about car insurance in India 2026, types of policies, benefits, coverage specifics, premium calculations and the claim process along with expert tips for choosing and best insurer.

What Is Car Insurance?

Car insurance is an contractual agreement between a car owner and insurer. With this contract, the policyholder pays a premium to receive financial protection against specified losses.

When your car gets in an accident, natural calamity damage or theft occurs, or you cause injury to another person or property with it, the insurance company pays for losses that are insurable under the policy.

Car insurance has 2 roles. It initially safeguards the owner of the automobile from incurring substantial costs concerning repairs and upkeep or replacement expenses. Second, it guarantees that victims aren’t shortchanged by third parties related to an accident.

One accident without insurance could leave you with large financial liabilities. Modern cars nowadays come with a host of sophisticated technology, along with more expensive replacement parts and labor charges have soared in many countries. Insurance facilitates effective risk management in such scenarios for the vehicle owner.

Why Car Insurance Is Important in 2026

India’s automotive space has changed drastically over the past few years. The big difference between today’s vehicles and that of yesteryear is the sophisticated electronics, advanced safety systems, sensors, cameras and connected technology found in modern cars. These features do make your car safer and more convenient to drive, but they make it way more expensive to repair.

Traffic congestion in urban cities is continuing to grow which increases the probability of small and large accidents. At the same time, many areas of the country have witnessed frequent extreme weather events like floods, heavy rain, cyclones and storms.

As far as situations like these are concerned, then car insurance serves as a buffer for the person financially. A good policy can cover the owners of the vehicle in case any repairs amounting to lakhs or even thousand rupees.

Insurance takes off the worry. By having coverage, policyholders don’t need to stress about any sudden expenses after an accident or natural disaster, they’ll be able to count on their insurer.

As for companies with company-owned vehicles, insurance also matters. It ensures continued operation of your business by minimizing the potential for loss of income due to car accidents.

How Car Insurance Works

For this reason, having a fundamental understanding of how car insurance works can be crucial to determining what kind of coverage is right for you.

By this, you buy a policy and pay the premium to the insurance company. In exchange, the insurer promises to cover certain risks stated in the policy document.

When an insured event occurs like an accident or theft you notify the insurer and make a claim. The insurance company then processes the claim, checks on the specifics of the claim and pays up to your policy limits for covered losses.

How much compensation will depend on:

- Type of policy purchased

- Coverage limits

- Insured Declared Value (IDV)

- Deductibles

- Nature of the damage

- Applicable exclusions

Say, for instance, your car gets damaged in an accident and is eligible for replacement loss coverage under your comprehensive policy; the insurer will pay for repairs or replacement less any deductible.

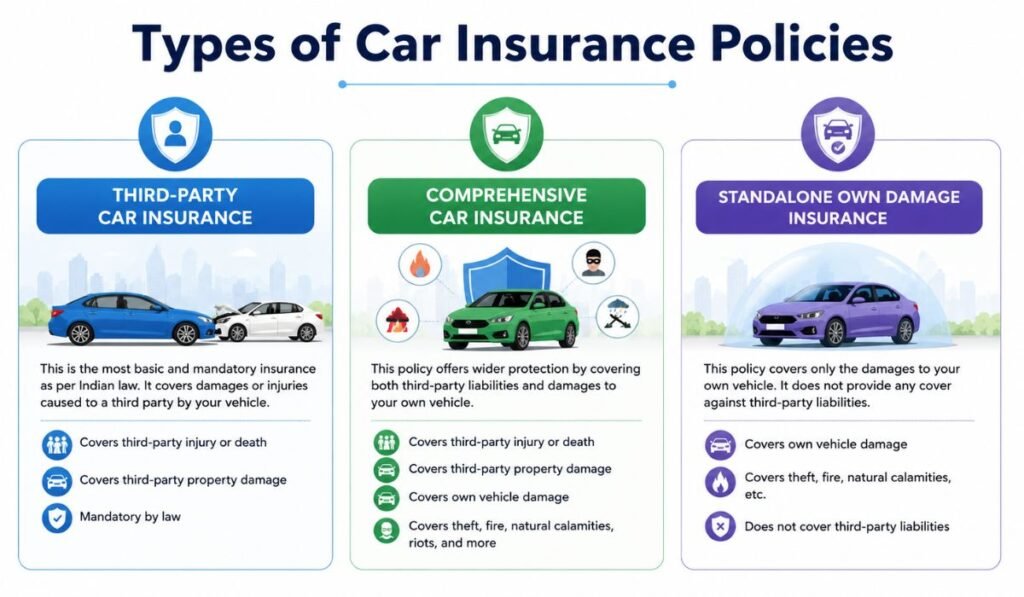

Types of Car Insurance Policies

Car insurance in India is well segmented into various categories wherever the distinct protection needs may be met.

Third-Party Car Insurance

Third-party insurance – This is the minimum insurance you must obtain by law. It covers legal fees due to the damage of third-party injury, death or property.

If your car hurts someone or damages another person’s property, the insurer pays compensation on your behalf according to the policy terms.

On the other hand, third-party insurance does not cover damages to your own vehicle.

Comprehensive Car Insurance

Comprehensive insurance provides wider protection. It provides liability coverage against third parties while maintaining cover for your own vehicle in different situations.

This form of policy typically only covers damage arising from:

- Accidents

- Fire

- Theft

- Floods

- Earthquakes

- Storms

- Riots

- Vandalism

Due to its extensive coverage, most vehicle owners opted for comprehensive insurance in 2026.

Standalone Own Damage Insurance

This would cover damage to your own car but not third party liability.

It is widely advisable for such car owners who have already been legally given third-party insurance coverage to take extra protection for their vehicle.

Third-Party vs Comprehensive Car Insurance

One of the more significant options during a car owner is choosing between third-party and comprehensive insurance.

| Feature | Third-Party Insurance | Comprehensive Insurance |

| Legal Compliance | Yes | Yes |

| Own Vehicle Damage | No | Yes |

| Theft Protection | No | Yes |

| Fire Coverage | No | Yes |

| Natural Calamity Cover | No | Yes |

| Add-On Covers | No | Yes |

| Premium Cost | Lower | Higher |

| Overall Protection | Limited | Extensive |

While third-party insurance is less expensive, full cover provides much better financial protection.

Key Benefits of Car Insurance

Car insurance is one of the great benefits to give financial protection. Repairs on a car can be costly, especially if some major part is damaged. Insurance helps alleviate the weight of these expenses.

One another, quite important benefit is compliance with the law. Insuring your car is not only lawfully essential, but without some competent insurance coverage penalties and hurdles can arise.

Insurance that covers the value of your car gives you protection against theft as well. Given that vehicle theft is still a problem in many Indian cities, this cover can come in handy.

Insurance also provides peace of mind while travelling. All of these things may not be a concern anymore whether you are commuting daily or going on long road trips and with the assurance that your vehicle is being protected.

With a robust network of garages, most insurers are providing cashless repair facilities. This allows policyholders to have their cars fixed without needing to pay the entire cost of the repairs upfront.

What Does Car Insurance Cover?

The basic plan, in its short form, typically includes more coverage for a comprehensive policy purchased is the type of protection involved or available.

Accidental damage is still amongst the most frequent claims within car insurance policies. You can read more in simple terms, and how the costs are covered if damage to your car occurs as a result of an accident with another car; For example, hitting a stationary object on the road or falling into an unexpected bump; In addition, as far as possible – due to medical discharge.

The second important feature is theft coverage. Where a vehicle is stolen and not able to be traced, the insurer pays the owner as per the relevant Insured Declared Value.

Comprehensive policies generally include coverage for natural disasters like floods, cyclones, earthquakes, land slides or storms. With extreme weather events continuing to affect different parts of India comes greater emphasis on this.

You also cover damage by fire like the accidental fires and explosions.

Moreover, riot, strike, and malicious and vandalism loss are generally what comprehensive policies also cover.

What Is Not Covered Under Car Insurance?

Car insurance is an important coverage that provides general protection against various damages to a vehicle, but there are exceptions in car insurance policies.

It’s not covered because normal wear and tear occurs with the use of a vehicle. Mechanical or electrical breakdown risks are usually not covered as well unless seperate addon covers have been taken out.

So, DUI claims will be rejected. Claims related to unlawful activities or driving a vehicle without a license will likely not be covered either.

Standard policies typically exclude damage caused as a result of war, nuclear events or other exceptional situations.

It is important to familiarize yourself with these exclusions as many claim disputes stem from unwarranted assumptions about what the insurance does not cover.

Important Add-On Covers in Car Insurance

A typical comprehensive policy is broad in scope but several insurers include optional add-on covers that can enhance your protection. With much more complex and costly components in modern vehicles, and the sophistication of technology systems that have an impact on repair costs, these add-ons are used especially during 2026.

Zero Depreciation Cover

Depreciation is accounted for in the insurance settlement process with a regular insurance policy. Which means when you replace any parts the insurer will subtract that depreciation value first and then payout on the claim.

In case you have opted for a Zero Depreciation Cover, the insurer will cover the invoice cost of all eligible parts without accounting for depreciation. This provides a notably higher claim settlement and lesser fosse pay-out for policyholders.

This add-on is especially useful for compact cars and luxury models.

Engine Protection Cover

Water ingress, oil leakage or hydrostatic lock leading to engine damage are generally not covered under regular insurance policies. Nevertheless, repairs to an engine can be some of the most costly automobile repairs.

Engine Protection Cover: Coverage for engine components damaged due to a listed eventuality, such as leakage of lubricating oil, frost damage etc.

This is a very useful and recommended add-on in flood areas.

Roadside Assistance Cover

Things break down, and no matter how well maintained a vehicle can be, mechanical trouble is always around the corner. Roadside assistance means help is there when you need it.

Typical services include:

- Towing assistance

- Flat tyre replacement

- Battery jump-start

- Fuel delivery

- Minor on-site repairs

- Locksmith assistance

This add-on can provide considerable assistance to drivers constantly making longer journeys.

Return to Invoice Cover

If you are unable to recover the vehicle, most insurers compensate on a Total Loss Basis and pay per Insured Declared Value (IDV).

Return to Invoice Cover: It covers the difference between the IDV and actual vehicle invoice value This ensures owners receive a larger payout when they need to replace their vehicle.

Consumables Cover

Standard policies usually do not cover individual repair related items like engine oil, coolant, nuts, bolts and washers or lubricant.

These are only a fraction of what the policyholder has to pay; Consumables Cover brings the policyholder savings on these charges, resulting in less impact from repairs and associated costs.

Understanding No Claim Bonus (NCB)

One of the most alluring attributes of car insurance is its ability to serve a No Claim Bonus. It favors policyholder who do not make a claim during the policy term.

If you have a claim-free year, the insurer gives you a discount on the renewal premium. The discount approaches becomes more higher by the ceilings of consecutive years.

Typical No Claim Bonus Structure

| Claim-Free Years | NCB Discount |

| 1 Year | 20% |

| 2 Years | 25% |

| 3 Years | 35% |

| 4 Years | 45% |

| 5 Years or More | 50% |

Someone who has not filed a claim for years could save substantially as a policyholder.

Something to note is you cannot take NCB on the vehicle, it belongs to the owner of the vehicle. In case of buying a new car, the accumulated NCB can be transferred to the new vehicle.

What Is Insured Declared Value (IDV)?

Simply put, the Insured Declared Value or IDV is the market value of the insured car.

The highest amount to be paid by the insurer when your vehicle is a total loss or stolen and is not recovered.

Because of depreciation, IDV comes down each year. Due to time decay, as the car gets older, its market value reduces and hence lowers the IDV.

Example of IDV Depreciation

| Vehicle Age | Approximate Depreciation |

| Up to 6 Months | 5% |

| 6 Months – 1 Year | 15% |

| 1–2 Years | 20% |

| 2–3 Years | 30% |

| 3–4 Years | 40% |

| 4–5 Years | 50% |

The right IDV selection. The lower your IDV, the less you may pay in premiums but with major claims, you face getting compensation that is pretty low.

Factors Affecting Car Insurance Premium

Not each vehicle owner is the same when it comes to car insurance premiums. Before determining the premium amount, insurers consider various factors.

Vehicle Make and Model

Luxury cars typically have higher insurance premiums because they cost more to fix or replace.

Insurance for a premium SUV or high-end sedan typically costs more than insurance for small hatchbacks.

Vehicle Age

IDVs are generally higher for newer cars so insurance premiums increase as well. This is because older cars tend to be cheaper, so the insurance payouts in case of an accident are lower.

Location

If you live in a metropolitan city, the premiums on vehicles are usually higher due to factors such as high car density and frequent accidents or thefts.

Type of Coverage

Comprehensive loss cover is more expensive than a third party product due to the wider scope of protection.

Add-On Covers

The more covers you add, the higher will the premium amount be. But these add-ons can be considerable depending on what the owner of the vehicle needs.

Claim History

No Claim Bonus discounts are offered to drivers who have a good track record without making an insurance claim.

Safety Features

You might save on premium with vehicles that have factory-installed anti-theft devices and advanced safety systems.

How Car Insurance Premium Is Calculated

Insurance pricing is based on a combination of regulatory “guidelines” and models to assess risk.

The premium generally consists of:

- Third-party premium

- Own damage premium

- Add-on cover charges

- Applicable taxes

Naturally, a vehicle with higher IDV, costly spare parts and other coverage will naturally demand an expensive premium.

Similarly, devices used against theft, voluntary deductible and earned NCB can decrease the premium.

Since every insurer adheres to a somewhat different pricing system, it is recommended by no means to skip studying quotes in fellowship with buying a policy.

Cashless vs Reimbursement Claims

Insurers today have two main ways to settle your claim.

Cashless Claims

With a cashless claim, the vehicle is fixed at one of the insurer’s network garages.

Then the damage that has been approved goes directly to the garage, which is then settled by the insurance company. The policyholder pays only for uncovered costs and deductibles.

Advantages include:

- Minimal paperwork

- Faster processing

- Reduced financial burden

- Convenient repair experience

Reimbursement Claims

A reimbursement claim works by the policyholder paying for repairs upfront and then creating invoices for the insurance provider to cover.

Insurer checks these documents and pays you for the claim amount, as described in the policy.

Reimbursement claims allow some flexibility in repairing facilities used, in general reimbursement usually requires more documentation and a significant processing time.

Car Insurance Claim Process

Digital platforms and mobile applications have made claim-filing a lot easier in 2026.

In general, the process starts a couple or a few weeks after the incident actually happens.

Step one: Make things safe and push the car to a safe location (if possible). Call for medical help and the police, if in fact injuries are involved.

Then, in a timely manner, notify the insurance company. By the most insurers, claims can be registered through mobile app, websites, call centers or WhatsApp services.

If need be, the insurer will hire a surveyor to inspect the damage. The surveyor inspects the vehicle and estimates for repair.

After the assessment write-up, you will enter repair mode. Settlement is done based on whether it was a cashless or reimbursement claim.

Documents Required for Car Insurance Claims

Requirements vary by insurer and claim type, but typical documents include

| Document | Purpose |

| Insurance Policy Copy | Policy Verification |

| Registration Certificate | Vehicle Ownership Proof |

| Driving License | Driver Verification |

| Claim Form | Claim Registration |

| FIR (If Required) | Theft or Major Accident Cases |

| Repair Bills | Expense Verification |

| Photographs | Damage Assessment |

Full and detailed documentation can help simplify the claims process.

How to Buy Car Insurance Online in 2026

Buying car insurance online is the first choice for most vehicle owners in India. It is quick and transparent, provides the opportunity to buyers to compare different insurers before they buy.

Step 0: Enter Basic Vehicle Details like Registration Number, Make, Model, Type of Fuel and year of manufacture. Insurers will then create policy options and premium quotations from these details.

Based on the available plans, policyholders can check coverage aspect to aspect with respect to claim settlement history, add-on options available, network garages and premium amount. This side by side, a real help for the buyer who can choose what is more appropriate coverage and price.

Once a plan is finalised, the buyer can tailor coverage with optional benefits like Zero Depreciation Cover, Engine Protection, Roadside Assistance, or Return to Invoice Cover.

You complete the payment using safe online channels and your policy document is generated within minutes electronically. Most of the time, insurance policies are stored electronically so you will not need a buffer for your documents.

Always, online buying has rendered insurance more accessible while also encouraging a lot of transparency related to pricing and policy features.

How to Renew Car Insurance

Renewing your car insurance is as vital as taking a new one. Letting a policy lapse means that the car owner is financially vulnerable and breaks the law.

Now most of the insurers remind you through email, SMS, and mobile app before the expiry of policy. Review own coverage before it’s time to renew

This is also an ideal time to compare policies from various companies. There may be better coverage, service or premium rates available elsewhere.

In case the person has been claim-free for the previous year, therefore this No Claim Bonus can be redeemed and applied while renewal to ensure that the premium is lower.

Renewing on time first ensures that you remain well protected and second, it helps avoid any unwanted complications which might arise due to lapses in policies.

How to Choose the Best Car Insurance Policy

Choosing car insurance is more than just picking the lowest premium. The cheapest of policies may not always yield maximum protection when the need is felt most.

The first factor is coverage. Most vehicle owners are well served by comprehensive insurance rather than basic third-party coverage, which is typically needed in order to be able to register an auto.

Reputation of insurers in settlement of claims also matters. A good insurer will help you with prompt claims processing and excellent support to make your life easier during a stressful time.

Evaluate network garages too. By building a really big cashless garage network, it brings more convenience and enables easier access to repair quality services.

Before finalizing a decision, it is recommended that policyholders thoroughly examine exclusions, deductibles and what add-ons they may be eligible for.

In the case of new cars, premium vehicles and electric cars, add-on covers often provide ancillary protection worth its hammer price.

The best insurance policy is the one that provides value, full coverage, and dependable customer service.

Top Car Insurance Companies in India 2026

India’s insurance market offers several reliable insurers with strong track records in customer service, claim settlement, and digital capabilities.

Leading Car Insurance Providers

| Rank | Insurance Company |

| 1 | New India Assurance |

| 2 | ICICI Lombard |

| 3 | HDFC ERGO |

| 4 | Bajaj Allianz |

| 5 | Tata AIG |

| 6 | SBI General Insurance |

| 7 | Reliance General Insurance |

| 8 | Oriental Insurance |

| 9 | National Insurance |

| 10 | United India Insurance |

Each insurer offers different strengths. Wherein some simply stress on competitive premiums, others rely heavily on digital services, cashless garage network and several add-on covers.

The decision is not necessarily linear and based on rankings, but simply what the owner of each vehicle needs.

Common Car Insurance Mistakes to Avoid

Numerous policyholders make unnecessary blunders, resulting in insufficient coverage or challenges when filing a claim.

For example, one of the worst mistakes is when you choose insurance only on the basis of premium amount. It’s good for you to do it when you save money but lack of cover comes later with high expenses.

Another common blunder is treating add-on coverages lightly. Some add-ons protect pretty well, especially on new and high-value vehicles.

Most vehicle owners also do not review the policy exclusions with any degree of scrutiny. Knowing what is not covered is as important as understanding what is covered.

Another complication can be a delay in claim notice. Insurers must be notified promptly following an incident.

Others ignore policy renewal altogether, living uninsured and in breach of their legal obligations.

Keeping these mistakes in mind can go a long way to help with avoiding them and making this part of your life so much smoother while allowing for proper financial protection.

The Future of Car Insurance in India

So much has changed in the car insurance world! Technological transformations are changing the way policies are purchased, managed and claimed.

AI applied for claim assessment, fraud detection and customer support. Now you can register a claim instantly via mobile apps and digital platforms, thanks to many insurers.

Telematics-based insurance is projected to become increasingly attractive in the coming years. This model would set premiums on actual driving behavior, unlike general risk categories. Perhaps little or no insurance cost but if ur late UR fine.

The market also is being reshaped by electric vehicles. With continued adoption of EVs, insurers have begun developing tailored policies designed to respond to battery-related risks and advanced technology components.

Insurance never has been more consumer-facing or efficient thanks to digital innovation, which is also creating products that are easier to understand.

Frequently Asked Questions (FAQs)

1. Is car insurance mandatory in India?

Yes. Legally, it is compulsory for every car running on public roads to at least have third-party insurance cover.

2. Which type of car insurance is best?

Full insurance is more comprehensive and covers not only third-party liabilities but also damage to the insured vehicle itself; Hence, its premium has a higher cost than third party insurance.

3. What is No Claim Bonus (NCB)?

No, A No Claim Bonus is a reward offered to policyholders for not making any claims during the tenure of the policy.

4. Does car insurance cover theft?

Most comprehensive car insurance policies offer coverage for the theft of an insured vehicle as described in the policy.

5. What is IDV in car insurance?

The IDV (Insured Declared Value) of the vehicle is also defined as your car’s current market price and it is used to calculate the compensation amount if an unfortunate total loss situation arises.

6. Can I transfer my insurance when selling my car?

Yes. An insurance policy can often be transferred to the new owner by following the procedures as per insurer policies.

7. Does insurance cover flood damage?

As far as flood-caused damage, it is typically covered except for exclusions in the policy.

8. What happens if my insurance policy expires?

There are penalties for driving without insurance, and the owner of the vehicle is financially exposed.

9. Can I buy car insurance completely online?

Yes. Most insurers allow policy purchase, renewal, claim registration, and policy management through digital platforms.

10. Is Zero Depreciation Cover worth buying?

Zero Depreciation Cover is very advantageous for brand new cars and luxury vehicles as it saves you from paying any repair expenses out of your pocket during a claim.

11. How can I reduce my insurance premium?

Keeping a clean-compromise history, installing anti-theft devices, choosing ideal deductibles and comparing insurers to see if any of them provide you hidden provides those can help in reducing premiums.

12. Are electric vehicles covered by car insurance?

Yes. Most insurance companies currently offer specific coverage options to electric vehicle owners, covering some components unique to EVs.

Conclusion

In 2026, car insurance is more than just a legal requirement. It is a necessary financial tool that provides protection to vehicle owners from accidents, thefts, natural calamities and third-party liabilities. As costly repairs, rising traffic density, and changing automotive technologies make it increasingly difficult to find the best auto insurance policy that meets your needs, this question has become essential.

Third-party insurance may only fulfill regulatory requirements, but such forms offer coverage that is much broader and unlike comprehensive insurances. These decisions can be complemented by taking coverages in different add-ons like — Zero Depreciation, Engine Protection and Roadside Assistance which will not only secure you but relieve financial stress at times of unexpected emergencies.

A thorough comparison of coverage details, the efficiency of claim settlements, network garages, customer service and premium cost is required to pick a right policy. With insights into how car insurance functions and with the coverage that best fits their needs, vehicle owners can better protect themselves from stress on every road taken—and financial devastation should an accident occur.

Regardless of whether you’re getting a new car, renewing an old policy or comparing insurers, taking a decisive step now can save you a considerable amount of time, money and stress down the road.