In an era marked by rapid technological change, the heightened proliferation of cybercrime, and political unrest across the globe, risk management has become a necessity – a core tenet of sustainable business strategy. The Corporate Insurance Policy is one of the most effective tools that a business can assert to protect any financial losses it may incur due to unexpected or unforeseen events. From a small startup to a large multinational enterprise, having the nitty-gritty knowledge of a Corporate Insurance Policy signifies the difference between surviving a crisis and permanently closing your doors.

This definitive guide is a One Stop Solution to Corporate Insurance Policy covering Its Definition, Types, Advantages, Coverage Information, Such as Exclusions and Inclusions of Corporate Insurance Policy With Important Questions Answered Lifetime – A one-stop solution.

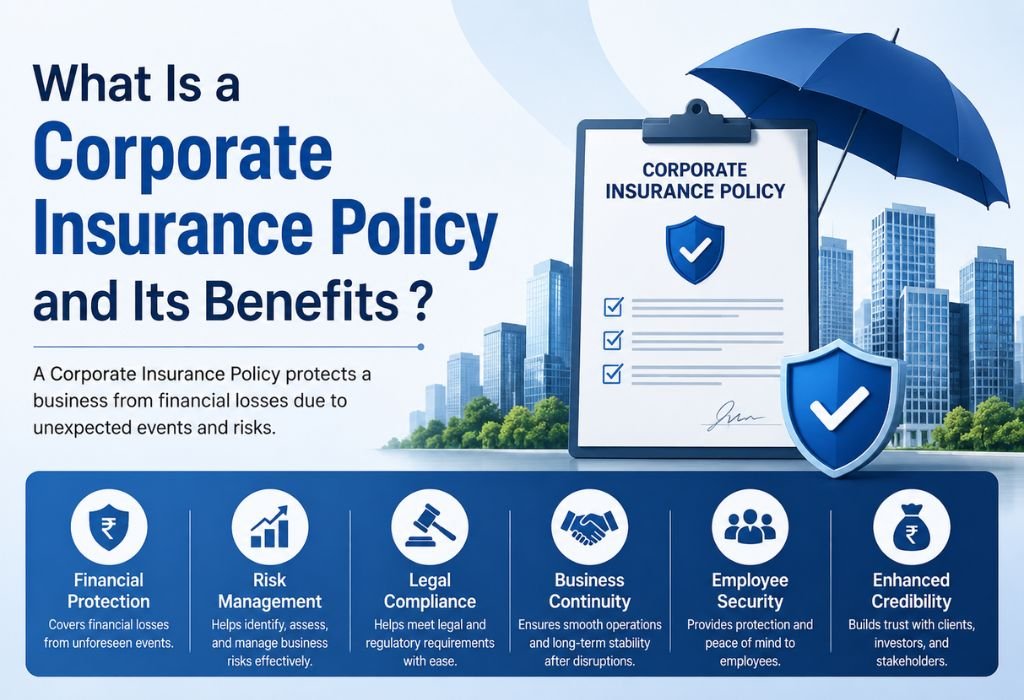

What Is a Corporate Insurance Policy?

Corporate insurance policy is a contract between the business (the insured) and an insurer where the insurer agrees to compensate an organization by payment of financial losses if they occur in exchange for regular premium payments. Through Corporate Insurance Policy, it is possible to deal with the complex and multi-dimensional problems that can arise every day in an organisation which a personal insurance cannot do.

Some of these risks can be property damage, employee-related liabilities, disputes potential from litigation, cyber threats, business interruptions and many more. A Corporate Insurance Policy typically consists of a well-tailored package of multiple lines, integrated into the overall risk profile and needs of the client.

Read Also:- What is the Right Age to Purchase a Health Insurance Policy?

Why Is a Corporate Insurance Policy Important?

From natural disasters to accidents and lawsuits, data breaches, businesses face a variety of risks. Even financially healthy organisation can be brought to their knees with a single incident without sufficient insurance coverage. A Corporate Insurance Policy:

- Safeguard corporate assets and reserves

- Protects employees and their families

- Meets all legal and regulatory obligations

- Build the business credibility among stakeholders and investors

- Ensures unbroken functionality following interruptions

- Reduces financial implications of litigation and liability claims

Types of Corporate Insurance Policies

A Corporate Insurance Policy can comprise several covers. Here is a summary of the most popular types.

| Type of Insurance | What It Covers | Who Needs It |

| General Liability Insurance | Third-party bodily injury, property damage, and advertising injury | All businesses |

| Property Insurance | Buildings, equipment, inventory, and physical assets | Businesses with physical assets |

| Workers’ Compensation | Employee injuries, illnesses, and lost wages from workplace incidents | All employers |

| Professional Liability (E&O) | Claims of negligence, errors, or omissions in professional services | Consultants, IT firms, lawyers |

| Directors & Officers (D&O) | Personal liability of executives for management decisions | Corporations with boards |

| Cyber Liability Insurance | Data breaches, cyberattacks, ransomware, and digital theft | Tech firms, e-commerce, healthcare |

| Business Interruption Insurance | Lost income and operating expenses during forced closure | Retail, manufacturing, hospitality |

| Commercial Auto Insurance | Company vehicles involved in accidents or theft | Businesses with company fleets |

| Product Liability Insurance | Injuries or damages caused by company products | Manufacturers, retailers |

| Group Health Insurance | Medical expenses for employees and their dependants | All businesses with staff |

| Key Person Insurance | Financial loss from the death or disability of a critical employee | SMEs, startups, partnerships |

| Trade Credit Insurance | Non-payment by customers or business partners | Exporters, B2B businesses |

Key Benefits of a Corporate Insurance Policy

One can reap long-term benefits by investing in a strong Corporating Insurance Policy for small, medium, and large size companies. Here are the major benefits:

Financial Protection Against Unforeseen Losses

The primary advantage of a Corporate Insurance Policy is monetary security. Disasters both natural, accident and intentionally inflicted can lead to enormous unanticipated expenditure. Insurance coverage helps to offset the full financial impact of such events turning up on the company’s balance sheet and maintains working capital and solvency in the long run.

Employee Protection and Retention

A Corporate Insurance Policy consisting of group health, workers’ compensation and life insurance coverage shows that the company cares about its employees. To compensate for this by satisfying legal requirements in most jurisdictions is, on the one hand, only a partial solution and greatly increases employee motivation, productivity and loyalty while reducing down costs through staff turnover.

Risk of Fine and Legal Compliance

In many countries around the world, a certain type of insurance like workers’ compensation and employer’s liability is legally required in specific sectors. The Corporate Insurance Policy covers the business to operate in complete accordance with local labour laws, sectoral regulations and contractual obligations; thus avoiding huge monetary penalties and legal consequences.

Business Continuity and Operational Resilience

Business interruption coverage (that which will keep cash flowing even when operations are halted don fire, flood or other covered event) is crucial in a Corporate Insurance Policy This allows for the payment of repetitive expenditures such as rent, salaries, and debt repayment when revenue fluctuates temporarily.

Enhanced Credibility and Stakeholder Confidence

A large number of clients, investors, banks and business partners usually prefer companies that are supported by securities coverage. A Corporate Insurance Policy is a sign of professional indemnity and gives you financial stability to help get work, gather investment or form partnerships more efficiently.

Protection from Cyber Threats

Accrual of Cyber liability policy in Corporate Insurance Policy being threatened by cyber attack have rendered services almost mandatory. It includes the expenses of notifying people about a data breach, credit monitoring services, legal defence (in case of lawsuits), fines from regulators, and even ransom payments forming an indispensable safety net in our digital age.

Insurance Protection for Litigation and Legal responsibilities

The customers, employees, competitors, or regulators can lead to legal comprise. Corporate Insurance Policy covers legal expenses, including court costs and settlement amount; so that no lawsuit can sink the company into either a cash shortfall or become representative of insolvency.

Tax Benefits

The insurance premiums must then be regarded as deductible business expenses corporations use to reduce their overall taxable income, which is conventional in most jurisdictions. It turns the Corporate Insurance Policy into not only a protective tool but also a tax-effective financial instrument.

Corporate Insurance Policy: Key Coverage Areas at a Glance

| Coverage Area | Typical Risks Covered | Benefit to Business |

| Property & Assets | Fire, flood, theft, vandalism, equipment breakdown | Replacement/repair without capital drain |

| Liability | Third-party injury, product defects, advertising errors | Legal cost protection |

| Human Capital | Workplace injury, illness, accidental death | Employee welfare & legal compliance |

| Professional Services | Errors, omissions, negligence claims | Reputation & financial protection |

| Cyber & Data | Hacking, data theft, ransomware, phishing | Regulatory compliance & recovery |

| Business Operations | Revenue loss from forced closures | Cash flow maintenance |

| Leadership | Executive decision-making disputes, wrongful acts | Board-level risk protection |

| Supply Chain | Supplier default, trade credit failure | Commercial continuity |

Factors That Affect the Cost of a Corporate Insurance Policy

Corporate Insurance Policy is not a fixed number the premium for this kind of policy varies depending on several risk factors related to business. An understanding of these can assist firms plan more effectively, negotiating rates and not over or under insuring.

Business Size and Revenue

Because they have greater financial exposure, typically larger businesses with higher revenues and more employees pay insurance premiums at a higher rate. Insurers determine premiums based on annual turnover, number of insureds (headcount) and asset value.

Industry and Risk Profile

Risks carried out by a manufacturing company will differ from those of a software firm. Corporate Insurance Policy premiums are higher in construction, chemicals and healthcare compared to more low-risk sectors like consulting or accounting.

Claims History

Insurers generally price companies where claims have a history of being frequent or especially large high risk will pay a higher premium. On the other hand, if you have a clean claims record, therefore insurers will usually offer discounts and no-claim bonuses.

Coverage Scope and Limits

Premiums are based on the scope of coverage (the extent to which a person or entity is covered), policy limits, and deductibles. The more extensive your policy is and the higher its limits, the more you’ll have to pay in premium.

Location

The business’s geographical area has an impact on the risks of natural catastrophes, crime statistics for the area, and regional litigation patterns all factors influencing the prices associated with a Corporate Insurance Policy.

Estimated Premium Ranges by Business Type

| Business Type | Estimated Annual Premium Range | Primary Coverage |

| Small Retail Business (10–20 employees) | ₹50,000 – ₹2,00,000 | Property, Liability, Group Health |

| Mid-size IT Company (50–200 employees) | ₹3,00,000 – ₹10,00,000 | Cyber, Professional Liability, D&O |

| Manufacturing Unit (100–500 employees) | ₹8,00,000 – ₹30,00,000 | Property, Workers’ Comp, Product Liability |

| Large Enterprise (500+ employees) | ₹25,00,000+ | Comprehensive Multi-line Policy |

| Healthcare Organisation | ₹10,00,000 – ₹50,00,000 | Professional Liability, Cyber, Health |

| Logistics & Transport Company | ₹5,00,000 – ₹20,00,000 | Commercial Auto, Cargo, Liability |

Note: Premiums are indicative estimates and vary by insurer, policy scope, claims history, and business-specific risk profile.

How to Choose the Right Corporate Insurance Policy

There needs to be a systematic approach to choose the right Corporate Insurance Policy. Here is a step-by-step process:

Step 1: Perform a Complete Risk Assessment

Know all the potential threats that your business is facing- operational, financial, environmental, technological and human. This assessment underlies your insurance strategy.

Step 2: Identify the Required Coverage

Understand your legal insurance needs based on your industry and location. Legislation may make workers’ compensation, employer’s liability and some professional indemnity coverages a legal requirement.

Step 3: Inventory Your Assets

Identify all business assets – buildings, machinery, intangible assets, stock and vehicles with suggested replacement cost and coverage.

Step 4: Compare Different Insurance and Brokerage Companies

A single quote is not enough to cover. Partner up with a corporate insurance broker who is knowledgeable and competent enough to be able to obtain quotes from numerous insurers and break down the fine print on each policy.

Step 5: Intensive Review of Policy Exclusions

All Corporate Insurance Policies include exclusions particular events or situations of cover. Asking about these exclusions will help ensure you are not caught off guard in the middle of a claim.

Step 6: Review and Update Each Year

As your business grows, so does your need for insurance. 1. Keep your Corporate Insurance Policy updated once every year or whenever there is a major change in how your business operates – e.g., hiring more employees, expanding operations, coming up with new products.

Common Mistakes Businesses Make with Corporate Insurance

| Common Mistake | Consequence | How to Avoid |

| Underinsuring assets | Insufficient payout in claims | Conduct regular asset valuations |

| Ignoring cyber coverage | Massive financial losses from data breaches | Add cyber liability to your policy |

| Not reading exclusions | Claim rejections on expected events | Review policy documents with a broker |

| Failing to update policy | Coverage gaps as business grows | Annual policy review mandatory |

| Choosing price over coverage | Inadequate protection when needed | Balance cost with coverage quality |

| Missing renewal deadlines | Lapse in coverage, legal penalties | Set automated renewal reminders |

| Not training employees | Higher workplace accidents, increased claims | Invest in safety programmes |

How to File a Claim Under a Corporate Insurance Policy

Getting the right coverage is equally crucial for filing a claim. When an insurable event happens, do the following:

- Notify your insurer or broker promptly after the occurrence most policies impose timing obligations on when you must notify them of an event.

- Collect evidence of the loss or damage using photographs, invoices and written reports.

- Do not attempt to repair or dispose of anything damaged before it has been inspected by the insurers surveyor.

- Send the actual claim form with any supporting documentation that your Corporate Insurance Policy requires.

- Fully cooperate with the investigation and assessment process of the insurer.

- Regularly track claim status and follow-up to ensure resolution in a timely manner.

Determine what basis is listed for the claim’s denial, and seek help from a broker or lawyer about challenging it.

Emerging Trends in Corporate Insurance Policy

Corporate insurance sector continues to evolve. 11 Key Trends that will define the future of Corporate Insurance Policies – An overviewCompanies must take notice of these factors impacting corporate insurance policies moving forward:

Parametric Insurance

Parametric insurance, conversely, pays out a predetermined amount when specified conditions manifest for example an earthquake of specific magnitude without the need for traditional loss validation and settlement speedier claim payouts for businesses.

ESG-Linked Insurance Products

Corporate insurance policy products are increasingly being designed by insurers to encourage businesses with favorable Environmental, Social and Governance (ESG) standards, lowering the premiums with which businesses are rewarded for strong performance in this area.

Artificial Intelligence in Risk Assessment

AI and big data analysis is allowing insurers to understand the risk profiles of businesses better, which means that premium for Corporate Insurance Policy can be highly perceived more personalized, priced competitively.

Pandemic and Business Interruption Coverage

After the COVID-19 pandemic, both insurers and corporate buyers of coverage have re-evaluated business interruption coverage, with pandemic-specific wording incorporated in new policies perhaps as one of emerging factors when measuring Corporate Insurance Policy.

Corporate Insurance Policy vs. Other Risk Management Strategies

Corporate Insurance Policy is the protection coverage in a more comprehensive manner, the policy ensures financial security against any risk that a corporation might retain due to unforeseen circumstances such as natural disasters. Although Self-Insurance, Avoidance and Safety Training might mitigate or avoid risks from occurring, they will not compensate you for large financial losses. Insurance protects against the unknown risks and thus, allows to stay in business. In the end, the most effective risk management strategy is to leverage insurance with factors that would mitigate risks in addition to protecting your company from extreme financial ruin.

| Strategy | Protects Against | Limitations | Best Used When |

| Corporate Insurance Policy | Wide range of financial losses | Premium costs; exclusions apply | Comprehensive, ongoing protection |

| Self-Insurance / Reserve Fund | Minor, predictable losses | Insufficient for catastrophic events | Low-frequency, low-severity risks |

| Risk Avoidance | Specific identified risks | Limits business opportunities | High-risk activities with no mitigation |

| Contractual Risk Transfer | Liability shifted to third parties | Depends on contract enforceability | Vendor/contractor relationships |

| Risk Reduction / Safety Training | Reduces frequency of incidents | Does not eliminate financial impact | Workplace safety and process improvement |

Frequently Asked Questions (FAQs)

Q1. What is the difference between a Corporate Insurance Policy and a personal insurance policy?

A: Personal insurance gives cover for individuals and their personal belongings, while Corporate Insurance Policy covers business assets, workforce, processes, liabilities and professional risks pertaining to an organisation.

Q2. Is a Corporate Insurance Policy legally mandatory in India?

A: Some coverages in a Corporate Insurance Policy are statutorily required in India. Legally mandated by the Employees’ Compensation Act (for workers’ compensation cover), certain sizes of employers are also required to purchase group health insurance (mandated by IRDAI), and third-party motor insurance is mandatory for vehicles used by the companies. Depending on your business type, other coverages are highly recommended.

Q3. Can small businesses benefit from a Corporate Insurance Policy?

A: Absolutely. SME are usually more exposed to financial shocks than their large counterpart. SMEs get low-priced, packaged corporate coverage under a Corporate Insurance Policy to protect against the same threats that could make them go out of business altogether.

Q4. What is a Business Owner’s Policy (BOP)?

A: A BOP is a Corporate Insurance Policy that combines general liability and property insurance into one affordable plan for small to mid-sized businesses. This is frequently one of the easiest and cheapest entry points to corporate applications.

Q5. How is the premium for a Corporate Insurance Policy calculated?

A: There are multiple factors that premiums depend on such as the type of business, commercial size, annual revenue and number of people you employ, risk profile by industry (the kind of coverage required), geographical location, different asset values in an event a claim is made against you at a certain limit(legal fees), average deductible amount per year before coverage kicks in etc.

Q6. Does a Corporate Insurance Policy cover pandemics or epidemics?

A: However, due to the impact of COVID-19, many insurers now provide dedicated riders for epidemics/pandemics. It is important to review your own policy wording and discuss this with your broker.

Q7. What is the claims settlement ratio and why does it matter?

A: The claims settlement ratio is the total number of claims settled by an insurer as a percentage of total claims (received in a year). A high ratio (more than 90%) suggests that this insurer is paying claims promptly, which should be of great significance when choosing your Corporate Insurance Policy provider.

Q8. Can a Corporate Insurance Policy be customised?

A: Yes. This varies, but most of the reputable insurers and brokers will allow you to lay out a Corporate Insurance Policy that is fine-tuned exactly to your needs in terms of risk exposure, budget, industry requirements & business size. Riders and add-ons can be attached to a base policy to create a fully personalized coverage plan.

Q9. How often should I review my Corporate Insurance Policy?

A: You should check your Corporate Insurance Policy at least once a year, and also when there are major changes in the way your business is operated new employees, assets, products or services offered by your company as well as entering new markets or restructuring the organisation.

Q10. What happens if I don’t have a Corporate Insurance Policy?

A: Operating without a Corporate Insurance Policy can be one of the financially disastrous decisions you will ever make in your business. Even one lawsuit, big fire, or data leak could potentially cost far more than the company can pay, leading it either to liquidation of its assets, a death spiral into debt, or just plain business failure. It exposes the business to statutory penalties where insurances are mandated.

Conclusion

Corporate Insurance Policy is not a luxury – It is an essential for business. With growing operational complexity, changing cyber risks, escalating litigation and global economic uncertainty: can your business afford a Corporate Insurance Policy? But better still: in the 2020s, could it possibly afford to operate without one?

A proper Corporate Insurance Policy can yield a lot, from financial security and employee wellness to legal protection and stakeholder confidence. This will allow your organisation to build a solid footing that can withstand whatever challenges come their way through careful consideration of business risks, choosing the appropriate types and levels of coverage, and working with a reputable broker.

However, to that end, take some time to assess your current quality of risk exposure then seek out a qualified corporate insurance advisor and ensure you hold a Corporate Insurance Policy which actually reflects the type of business you run. It costs every rupee that you pay as premium but the safety and peace of mind worths every penny.